Typical Normal (Gaussian) Distribution; Source

Normal distribution (Gaussian distribution) is one of the most important concepts.

Whenever we run a model or perform data analysis, we need to check the distribution of the dependent variable and independent variables and to see if they are normally distributed. If some variables are skewed or not normally distributed, it will affect the accountability of significant factors.

The variable that should be normally distributed is prediction error.

$\text{Y} = \text{Coef} * \text{X} + \text{C} + \text{Error}$

Simple linear regression equation

If the prediction error is normal distribution with the mean of zero, the siginificant factors conlcuded from the regression is reliable. However, if te the distribution of error significantly deviates from the mean of zero and not being normally distributed, the factors that we choose to be significant may not actually be significant enough to contribute to the output y.

To select the significant predicting factors, after we have constructed a model and prediction, we should plot a chart to see the distribution of prediction error.

# create a normal distributed data and non-normal data

import numpy as np

from scipy import stats

sample_normal=np.random.normal(loc=0, scale=4, size = 1000)

sample_nonnormal = stats.loggamma.rvs(c= 5, loc=0, scale=1, size=1000, random_state=1) + 20Test normality

To test normality of data, we can plot distribution plot, QQ-plot or using Shapiro-Wilk test

(1). Distribution plot:

Simply plot the distribution curve and see whether the plot follows bell curve shape. Non-normal sample is clearly left tailed.

import seaborn as sns

import matplotlib.pyplot as plt

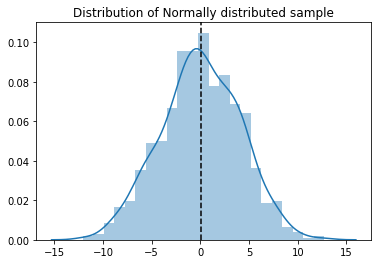

sns.distplot(sample_normal)

plt.axvline(x=np.mean(sample_normal), color='k', linestyle='--')

plt.title('Distribution of Normally distributed sample')

plt.show()

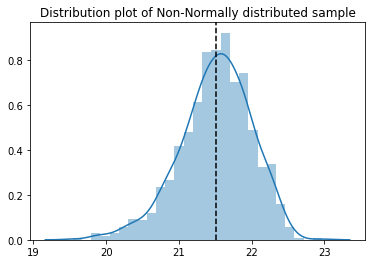

sns.distplot(sample_nonnormal)

plt.axvline(x=np.mean(sample_nonnormal), color='k', linestyle='--')

plt.title('Distribution plot of Non-Normally distributed sample')

plt.show()

(2). Shapiro-Wilk test:

Use the Shapiro-Wilk test, based on decided p-value threshold, usually we reject H0 at 5% significance level meaning if p-value is greater than 0.05 then we accept it as normal distribution:

PS: If sample size is greater than 5000, you should use test statistics instead of p-value as the indicator to decide.

# null hypothesis: the data was drawn from a normal distribution

test1= stats.shapiro(sample_normal)

test2 = stats.shapiro(sample_nonnormal)

print ('Test Statistics: {}\nP-value: {}\nFail to reject H0: the data was drawn from a normal distribution\n'.format(test1[0], test1[1]))

print ('Test Statistics: {}\nP-value: {}\nReject H0: the data was not drawn from a normal distribution\n'.format(test2[0], test2[1]))Test Statistics: 0.9982317686080933

P-value: 0.3935606777667999

Fail to reject H0: the data was drawn from a normal distribution

Test Statistics: 0.9849225282669067

P-value: 1.2197391541235447e-08

Reject H0: the data was not drawn from a normal distribution

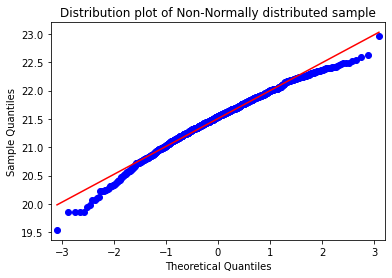

(3). QQ-plot: Very popular plot to see whether the distribution of data follow normal distribution.

import statsmodels.api as sm

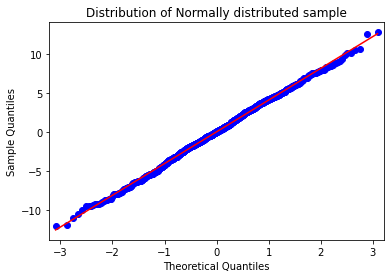

fig = sm.qqplot(sample_normal,line='s')

plt.title('Distribution of Normally distributed sample')

plt.show()

fig = sm.qqplot(sample_nonnormal,line='s')

plt.title('Distribution plot of Non-Normally distributed sample')

plt.show()

Fix the normality issue

Usually there are 2 reasons why this issue (error does not follow normal distribution) would occur:

- Dependent or independent variables are not normally distributed (based on skewness or kurtosis of the variable)

- Existence of a few outliers/extreme values which disrupt the model prediction

The solution for those are:

- Remove

outlierfrom bothdependentandindependent variables - Transform some non-normal variables to normal by using transformation function, such as

box-cox transformation

Below is the mathematic formula for Box-Cox transformation. Lambda value will be decided based on the data points to provide the best normal distribution shape after the transformation. We can directly use Python package to help us transform the data.

$ \begin{equation} y_i^{(\lambda)}= \begin{cases} \frac{y_i^{\lambda}-1}{\lambda} & \text{if $\lambda \neq 0 $,} \\ \ln y_i & \text{if $\lambda = 0$} \end{cases} \end{equation} $

#transform the data using box-cox transformation

sample_transformed, lambd = stats.boxcox(sample_nonnormal)

#plot the distribution curve and QQ-plot for transformed data

sns.distplot(sample_nonnormal)

plt.title('Distribution plot of Non-Normally distributed sample')

plt.axvline(x=np.mean(sample_nonnormal), color='k', linestyle='--')

plt.show()

sns.distplot(sample_transformed)

plt.title('Distribution plot of transformed Non-Normally distributed sample')

plt.axvline(x=np.mean(sample_transformed), color='k', linestyle='--')

# plt.ylim(bottom = 0 , top = 0.001)

plt.show()

fig = sm.qqplot(sample_transformed,line='s')

plt.title('QQ-plot of Non-Normally distributed sample')

plt.show()

print("Shapiro-Wilk test\n")

test3= stats.shapiro(sample_normal)

print ('Test Statistics: {}\nP-value: {}\nFail to reject H0: the data was drawn from a normal distribution\n'.format(test3[0], test3[1]))![]()

![]()

Shapiro-Wilk test

Test Statistics: 0.9982317686080933

P-value: 0.3935606777667999

Fail to reject H0: the data was drawn from a normal distribution

Although the transformed non-normal distribution looks a bit weird, according to the Shapiro-Wilk test and QQ-plot, we can see that the non-normal distributed sample is normally distributed after the box-cox transformatio.

In conclusion, if you try to find significant predicting factors or define the confidence interval, please remember to check the distribution of the error term after the model has being built.

If dependent variables or independent variables are not normal distributed then we can use box-cox transformation to transform it to make error term more normally distributed.

Except for the normality statistical assumption, there are other statistical assumptions in regression model, such as Multi-Collinearity in Regression.